The Hidden Costs of

Organizational Dishonesty

A

brief scanning of The Wall Street Journal — or, tellingly, almost any

other newspaper in the country — reveals the alarming prevalence and

far-reaching impact of organizational dishonesty. Reports of malfeasance or

criminal conduct in corporate governance, accounting practices, regulatory

evasions, securities transactions, advertising misrepresentations and so on

have become all too commonplace. It’s no wonder that business schools across

the country have been rushing to design and introduce courses that emphasize a

subject traditionally given short shrift: ethics.1

This

is not to say that, as a group, business people are inherently unethical. All

other things being equal, most executives would unhesitatingly choose the high

road. Except in hypothetical situations, however, all other things are never

equal. In any organization, people are motivated by myriad factors — sales

quotas, corporate economic health and survival, competitive concerns, career

advancement and so forth — which can easily override their moral compasses.

Indeed, in spite of the assortment of arguments contending that “ethics pays,”2 the number and extent of the recent

transgressions suggest that a significant portion of the business world has yet

to be persuaded.

Of

course, companies should always adhere to universal ethical principles because,

after all, that’s the right thing to do. But one additional reason for

businesses to engage in honest practices is that the consequences of failing to

do so may be much more harmful to the bottom line than has traditionally been

recognized. Companies that deploy dishonest tactics typically do so as a means

of increasing their short-term profits, and in that regard they might succeed.

But the misconduct is likely to fuel a set of social psychological processes

with the potential for ruinous fiscal outcomes that can easily outweigh any

short-term gains. In other words, organizations that behave unethically will

find themselves heading down a slippery and dangerous fiscal path.

In

this article we chart that path, providing details of the extent of the damage

and its insidious nature. Our formulation begins with a fundamental assertion:

An organization that regularly teaches, encourages, condones or allows the use

of dishonest tactics in its external dealings (that is, toward customers,

clients, stockholders, suppliers, distributors, regulators and so on) will

experience a set of internal consequences. These outcomes, which we call

malignancies, are likely to be surprisingly costly and particularly damaging

for two reasons. First, they will be like tumors — growing, spreading and

eating progressively at the organization’s health and vigor. Second, they will

be difficult to trace and identify via typical accounting methods as the true

causes of poor productivity and profitability. Thus, they might easily lead to

expensive misguided efforts that fail to target the genuine culprits of the

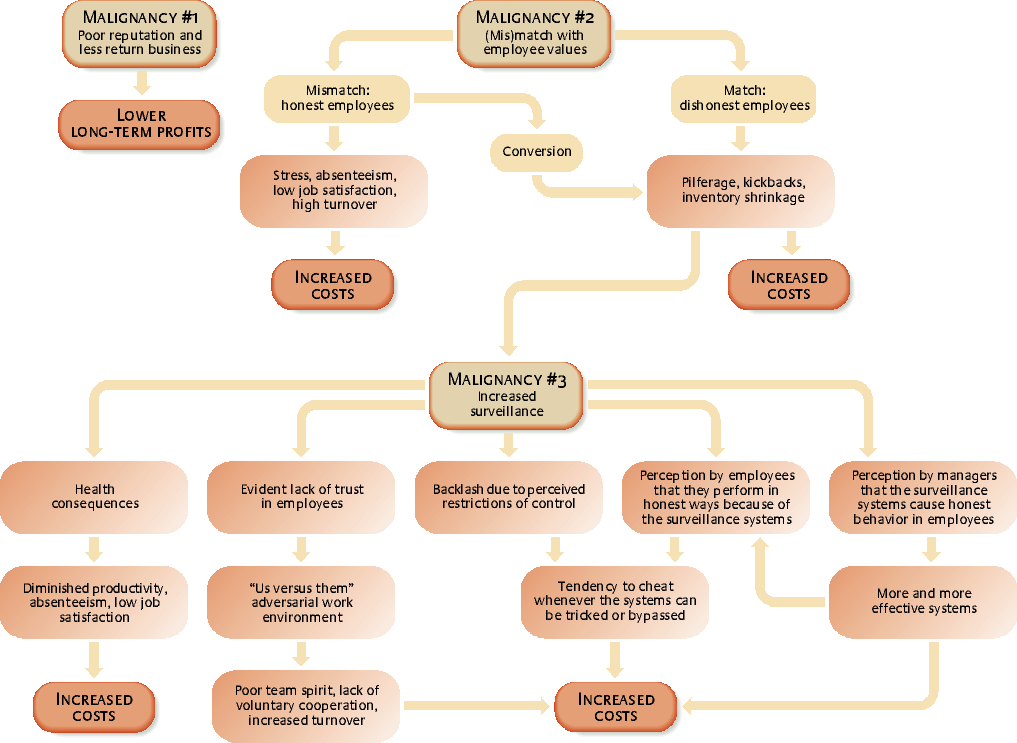

dysfunction. The malignancies can be categorized into three types, according to

the processes involved (see “The Consequences of Organizational Dishonesty”).

The Consequences Of Organizational Dishonesty

The Consequences of Organizational Dishonesty

A company with dishonest business practices toward

customers, vendors, distributors and other outsiders might achieve higher

short-term profits, but it would incur various costs from three types of

malignancy.

Malignancy #1: Reputation

Degradation

Perhaps

the most obvious consequence of systematic organizational dishonesty is that a

company will develop a poor reputation among current and prospective clients

and business partners. To be clear, we are not referring to small-scale,

localized or infrequent ethical infractions but rather to an organizational

culture in which employees are socialized into an environment that either

implicitly condones or, worse, explicitly teaches dishonest business practices.

When anyone outside the company (such as customers, partners, suppliers,

regulators or the media) uncovers the improper tactics, the fallout can be

swift and devastating. As Edson W. Spencer, the former chairman of Honeywell

Inc., once stated, “The businessman who straddles a fine line between what is

right and what is expedient should remember that it takes years to build a good

business reputation, but one false move can destroy that reputation overnight.”3

For

one thing, the damage to the firm’s opportunities for new and repeat business

can be considerable. According to a recent survey of the general public

conducted by Wirthlin Worldwide of Reston, Virginia, 80% of respondents stated

that their perception of the ethicality of a particular company’s business

practices has had a direct effect on their decisions to purchase goods or

services from that firm.4 And the financial damage could extend

further. According to the Wirthlin survey, 74% of the respondents asserted that

their perceptions of the honesty of a corporation’s behavior had also

influenced their decisions about whether to buy that company’s stock.5

More

importantly, the damage could be irreparable. An organization that has

historically been successful but is currently suffering from inefficient

operations, a lack of creativity or even incompetence still has the ability to

regain people’s confidence by demonstrating the early stages of a turnaround

(for example, by hiring a well-respected consulting group, by developing an

alliance with a highly regarded organization or by impressing industry insiders

with an innovative new product line). But companies that are perceived to be

corrupt will find it much more difficult, if not impossible, to shed themselves

of that stigma. Past research has found that, by nature, people react more

adversely to deceitfulness than to any other attribute.6 And even if only one branch of a

company is caught in the wrongdoing, the whole organization might suffer

because dishonesty is a trait that, when discovered in one domain, is

immediately perceived to be underlying the behaviors across other domains.7

Consequently,

once outsiders perceive that dishonest policies and practices have become

central to the way a company does business, that organization will face a long,

uphill battle. Research suggests that a disreputable company attempting to

recover lost trust needs to demonstrate its newfound integrity consistently on

numerous occasions (many more than the number taken to display its dishonesty

in the first place) to stand even a chance of convincing wary others that it

has changed for the better.8 During the recovery process, which

could easily take years, customers and clients who have defected are likely to

commit themselves to another, more respectable, organization. To speed its

rehabilitation, a company may need to replace top management quickly in an

effort to convince others of its sincerity and eagerness to attack the root

cause of the dishonesty.

Malignancy #2: (Mis)matches

Between Values of Employee and Organization

The

extent to which the values of an organization coincide with those of its

employees is another issue. Whether that match is good or not, companies with

dishonest practices are likely to incur substantial costs.

A Poor

Fit for Organizational Dishonesty

An

organization that encourages deceptive business practices by rewarding the use

of duplicity with outside contacts is likely to be met with moral opposition by

a number of employees whose values do not comport with those espoused by the

company. Many of these individuals will find their moral standards continually

clashing with workplace expectations, leading to constant stress from the

ever-present conflict.9 The resulting costs to the

organization can be considerable: greater instances of illness and absenteeism,10

lower job satisfaction,11 decreased productivity and higher

turnover.

Increased absenteeism.

Corporate

expenditures on illness and absenteeism amount to far more than the costs of

“get well” cards and Mylar balloons. A recent survey on unscheduled absences in

the workplace revealed an all-time high of $789 per employee annually, which

amounts to more than $3.6 million in yearly losses for larger corporations.

This number reflects only the direct payroll costs for the absent employees. It

does not include the cost of lost productivity and the expense of covering for

the absent individuals, including overtime pay for other employees and the

hiring of temporary workers.12

Lower job satisfaction.

An

even greater concern arises when the mismatch between the moral standards of

some employees and the unethical practices of a company leads to lower job satisfaction

among those individuals. From a strictly utilitarian perspective, an

organization should be concerned about worker job satisfaction only to the

extent that it affects employee productivity and turnover. Clear evidence has

existed for the latter (to be discussed shortly) but not for the former until

relatively recently. Specifically, traditional studies on the relationship

between job satisfaction and productivity suggested only a weak connection

between the two.13 But subsequent research has qualified

this finding, revealing that the correlation between job satisfaction and

performance is rather weak only for workers with low skill levels, presumably

because those individuals do not have the capability to produce high-quality

work even when they are quite content with their jobs.14 But for employees who are highly skilled,

job satisfaction actually makes a substantial difference: Those who were

satisfied with their jobs outperformed those who were not by a margin of 25%.

These

findings have serious implications. When moral employees are required to engage

in immoral behaviors, the productivity of the most competent and proficient

workers will suffer most. This outcome should be extremely troubling to many

organizations for two reasons. First, companies generally earn a sizable

portion of their revenues (and enhance their reputations) based on the highest

efforts of their ablest workers. If those individuals aren’t motivated,

revenues (and reputation) could easily suffer. Second, because the most capable

workers are usually the ones better able to find other jobs, dishonest

companies bear a large risk of losing their best employees.

Higher turnover.

Because

of the high direct costs of recruiting and training new employees, any

organization should be concerned if it has trouble retaining people. Dishonest

companies should take particular note, though, because their turnover will be

selective in nature. Research has shown that workers who do not share the

values of their organizations tend to be less satisfied with their jobs, less

committed to their organizations and significantly more likely to quit.15 Thus, over time, an unethical

corporation is likely to have employees who are disproportionately dishonest.

Moreover, policies that promote dishonest business practices are likely to

drive the most productive workers into the offices of more honest competitors,

where those individuals can find greater job satisfaction and be more at ease

with their work environments. In other words, once a dishonest organization has

unwittingly thrown out the baby, all that will be left is the dirty bath water.

A Good

Fit for Organizational Dishonesty

We

have already discussed how honest workers select themselves out of dishonest

firms by leaving to work for companies with values more consistent with their

own. It should be noted that this “moral dilution” also occurs at an earlier

point in the employment process. Specifically, job seekers tend to be attracted

to organizations with attributes that are congruent with their own personality

profiles.16 For example, in a recent survey, 76%

of respondents said that their perceptions of a company’s integrity would

influence their decision about accepting a job there.17 Of course, selection through the

filter of value congruency also occurs on the employer’s side. That is,

companies that regularly require their workers to engage in unethical practices

tend to seek people who are willing (if not eager) to play ball in that system.

As these various forces attract unethical prospects and repel ethical

employees, the low standards of a dishonest organization can be self-reinforced

in perpetuity.

Unethical

corporations do not merely select and retain dishonest employees; they create

them as well. Honest employees can be converted into wrongdoers in various

ways, but the process often begins with peer pressure or a supervisor’s direct

request.18 After transgressors have had the

opportunity to reflect on their recent misconduct, the incongruity between

their values and behavior will strongly motivate them to rationalize their

actions. (Otherwise, they would need to change their views of themselves in

light of what they’ve just done.) Counterintuitive as it may sound, many of

these individuals will continue to engage in dishonest business practices in an

attempt to bring a sense of legitimacy to their original offenses. These

workers are likely to find further comfort in the vast system of justifications

embedded in the corrupt ideology of the organizational culture.19 As the practice of rationalizing their

misdeeds becomes routine, the employees gradually adopt that ideology for

themselves.20

Regardless

of whether a company’s dishonest workforce comes primarily from turnover,

recruitment or conversion, an organization that consists of dishonest workers

is certain to suffer from various internal consequences, such as employee

theft, fraud and delinquency. After all, if workers are cheating customers and

others outside the company, why shouldn’t they also be bilking their employer?

Consider

the experiences of a former employee of a consulting firm whose manager

suggested that she withhold information from a client. “I was constantly on

guard to what I was ‘supposed’ to tell them,” says the former employee. “I felt

dishonest.” Later, the employee found herself regularly cheating on her travel

expenses. “We were allotted a set amount of money per day that was the maximum

we would be reimbursed for,” she recalls. “I began charging this amount to my

expenses each day, regardless of my actual expenses. This was the accepted

practice for most people on the project, but it was unethical.” Since leaving

the firm, the employee has had some time to reflect on her actions. “Looking back,”

she says, “I have to wonder if the dishonesty that I felt at the client site as

a firm representative had anything to do with the ease with which I was able to

be dishonest with the firm in another way.”

According

to a recent survey, fraud perpetrated by employees is the most common type of

fraud that afflicts companies. In fact, it is nearly twice as widespread as

consumer fraud, the next most prevalent type.21 The financial burdens of internal

fraud, including employee theft, are mind-boggling. According to the

Association of Certified Fraud Examiners, U.S. companies lose roughly $400

billion dollars a year to internal fraud.22 Years ago, a government legislative

committee noted that nearly one-third of all business losses in the United

States were the result of internal larceny.23 More recently, in 2003 nearly

two-thirds of corporations surveyed reported they had suffered from employee

fraud, and the trends suggest that the situation is likely to worsen.24 For example, compared with data from

half a decade ago, theft of company assets has more than doubled,

expense-account abuse has nearly tripled and fraud through collusion between

employees and third-parties is also on the rise.25

In

response to this growing problem, many organizations have overlooked any role

that their own dishonest policies and practices might have played. Instead,

they have focused on the symptoms of the problem, implementing a host of

specific preemptive and reactive measures. Of these, the use of stronger

internal controls, such as increased security and more sophisticated

surveillance systems, is growing at the fastest pace.26 But the unintended consequences of

such countermeasures can sometimes be nearly as deleterious as the problems

they are aimed at solving in the first place.

Malignancy #3: Increased

Surveillance

The

direct expenses associated with the installation of surveillance systems are

staggering. Between 1990 and 1992, for example, more than 70,000 U.S.

corporations spent over half a billion dollars on surveillance software.27 But the indirect costs —degradation of

the work environment that leads to adversarial relations between employer and

workers, diminished productivity and other dysfunctions — can also be

considerable.

Health

Consequences

Employee

monitoring is associated with a host of mental health problems,28

including high levels of tension, severe anxiety and depression.29 Employees are also more likely to experience

physical disorders, such as carpal tunnel syndrome, when they perceive their

organization’s surveillance system as encroaching on their privacy.30 These types of psychological and

physical ailments are linked directly to increased absenteeism and diminished

productivity.

Lack of

Trust in Employees

Workers

often perceive the installation of surveillance software and other devices as

clear indications that their organization doesn’t trust them. This perception

eventually harms any existing companywide esprit de corps, often creating an

atmosphere of antagonism between employees and management.31 In addition, workers who feel insulted

that their integrity is being questioned are more likely to quit or retaliate

with a variety of counterproductive behaviors, ranging from the simple

withholding of voluntary support to outright acts of revenge and sabotage.32 This type of dysfunctional environment

has been described by a former manager of a company that was trying to curtail

inventory shrinkage due to employee theft: “Senior management brainstormed the

best way to solve the issue and came up with the use of expensive video

surveillance equipment in the stockrooms to monitor employees leaving and also

the process of opening new shipments. This implementation did not decrease

shrinkage, but did have a negative impact on employee turnover.”

Backlash

to Perceived Restrictions of Control

People

who feel that their sense of freedom is being threatened will often try to

reassert some control over their environment.33 In the workplace, employees might

attempt to empower themselves through both corrective and retributive means —

that is, by trying to regain the control that was previously taken away and by

committing deliberately hostile actions to retaliate.34 Consequently, in an organization with

excessive control systems, some employees might be more motivated to steal from

the company.35 Of course, employee theft and other

dishonest behaviors are only likely to motivate management to procure even

higher levels of surveillance technology, further perpetuating the vicious

cycle.

Undermining

of Positive Behavior

Another

potential consequence of surveillance equipment is that many employees might

come to believe that the systems are warranted even when they’re not. That is,

honest and dishonest workers alike might assume that the monitoring must

reflect both the corrupt dispositions of fellow employees and the large rewards

of cheating. Unfortunately for the company, actions that convey expectations of

wrongdoing (either implicitly or explicitly) may in fact lead to a rise in

misconduct for both honest and dishonest workers by creating self-fulfilling

prophesies for the former36 and self-perpetuating ones for the

latter.37

Surveillance

technology can also undermine employee behavior in subtler ways. Specifically,

when individuals are being monitored closely, they might begin to attribute any

of their honest behavior not to their own natural predisposition but rather to

the coercive forces of the controls. Eventually, they might view their actions

as being directed less by their own moral standards and more by the prying eyes

of management.38 When that happens, they might lower

their ethical standards and be more inclined to try to outwit or elude the

surveillance system and engage in misconduct when they aren’t being monitored.39 This, too, will spur supervisors to

find more effective (and more expensive) control systems.

Overestimated

Influence of Monitoring

Management,

too, can begin to overestimate the power of surveillance systems. That is,

people who are responsible for the implementation, maintenance and

strengthening of control systems are likely to assume that the desirable

conduct of the monitored workers is primarily a result of the surveillance

equipment even when that behavior would have occurred without the use of such

systems.40 This misconception may help explain

why internal controls continue to rise in popularity in corporate America

despite the dramatic increases in supervisors’ workloads when new systems are

first established.41 After these systems are in place,

management may come to see them as more effective and more vital than they

truly are. And once again such mistaken assumptions might lead to greater

expenditures to purchase even more sophisticated systems.

Toward the Honest

Organization

Beyond

moral grounds, we have discussed sound utilitarian reasons for organizations to

conduct themselves ethically. We focused primarily on what the costs might be

for those businesses otherwise tempted to teach, condone or merely allow the

systematic use of dishonest practices with external contacts.

Although

many of the effects of organizational dishonesty are difficult to trace, the

damage done is no less real. Consider the following account of how the

unprincipled practices of a company helped cost it nearly $1 billion in losses.

According to a former employee, “The CEO … abused ethical principles on a

regular basis. … People believed him in the short run, but as the truth would

leak out, the company’s reputation deteriorated. Few companies are willing to

do business with him now — those that do will only do so on onerous terms.”

Eventually,

that culture of dishonesty had permeated the entire organization. “The

marketing department was coerced to exaggerate the truth,” says the former

employee. “The PR department wrote mostly false press releases, and salespeople

coerced customers.” Moreover, the misconduct was directed internally as well as

externally. “Taking a cue from the executives, employees would steal from the

company whenever they could, usually via travel and expense reports. Some would

cut side deals with suppliers,” recalls the employee.

To

make matters worse, a security force was hired to roam the building routinely,

ostensibly to protect employees, but many workers instead felt that they were

being spied on. That suspicion only intensified when reports of even minor

infractions, such as people taking long smoking breaks, were sent to the CEO.

Not surprisingly, job satisfaction at the company was bad, morale terrible and

turnover high. “People were attracted to the company by high salaries, which

the CEO saw as justification for treating employees poorly, but left as soon as

they could find work elsewhere,” recalls the former employee.

The

various costs of organizational dishonesty — decreased repeat business, low job

satisfaction and performance, high worker turnover, employee theft, expensive

surveillance mechanisms and an atmosphere of distrust — have often been cited

as severe business problems. But many organizations have failed in their

efforts to address those issues, often because they are unaware of a root

cause: their own tendencies to conduct business with customers and others

unscrupulously. So, instead, corporations often launch wrongheaded efforts to

control one fiscal hemorrhage (for example, losses from employee theft) by

creating another (namely, investments in increasingly expensive security systems).

The

more effective solution is to staunch the wound at its self-inflicted site,

with an unblinking examination of corporate dishonesty and a true commitment to

end it. But achieving ethical standards requires more than just implementing

institutional codes of conduct42 or more effective security systems

because increased control often leads only to even more negative outcomes.

Instead, the effort must begin at the top, with senior executives setting the

right example and then implementing policies to encourage the same behavior

from employees in their dealings with clients, customers, vendors and distributors

as well as with other employees. For example, top managers should incorporate

customers’ ratings of the ethicality of specific employees into the incentive

structures of those individuals. Also, the ethical reputation of the

organization as a whole should be measured regularly and included in the annual

assessments of the company’s performance. With such policies in place,

companies can maintain high standards of conduct and attract (and retain)

honest employees, and by doing so they can avoid the various hidden costs of

organizational dishonesty.

References

1. A. Sachdev, “Ethics Moves to Head of Class,” Chicago Tribune,

Friday, Feb. 14, 2003, Business Section, p. 1.

2. For a discussion of the history of “ethics as enlightened

self-interest” arguments, see A. Stark, “What’s the Matter With Business Ethics?”

Harvard Business Review 71 (May–June 1993): 38–48.